Buy-side expectations for corporate access under MiFID II

What do investors think about the new regime? Charles Hamlyn sets out the results of research, conducted jointly with the IR Society, into fund manager perspectives on corporate access, just before MiFID II became law.

Prior to MiFID II being implemented in January 2018, the European Securities and Markets Authority (ESMA) made it clear that in future investors would have to pay a ‘separately identifiable charge’ for any service, provided by an investment firm (broker), that affords a ‘material benefit’ to the recipient, including corporate access. They also made clear that responsibility for compliance rests firmly with the buy side.

So how is MiFID II expected to impact corporate access from the investors’ perspective? In partnership with the IR Society, QuantiFire undertook a research project to find out. Based on the responses of 302 investors (including 50% of the top 20 investment firms globally), our findings are summarised below.

The way things were

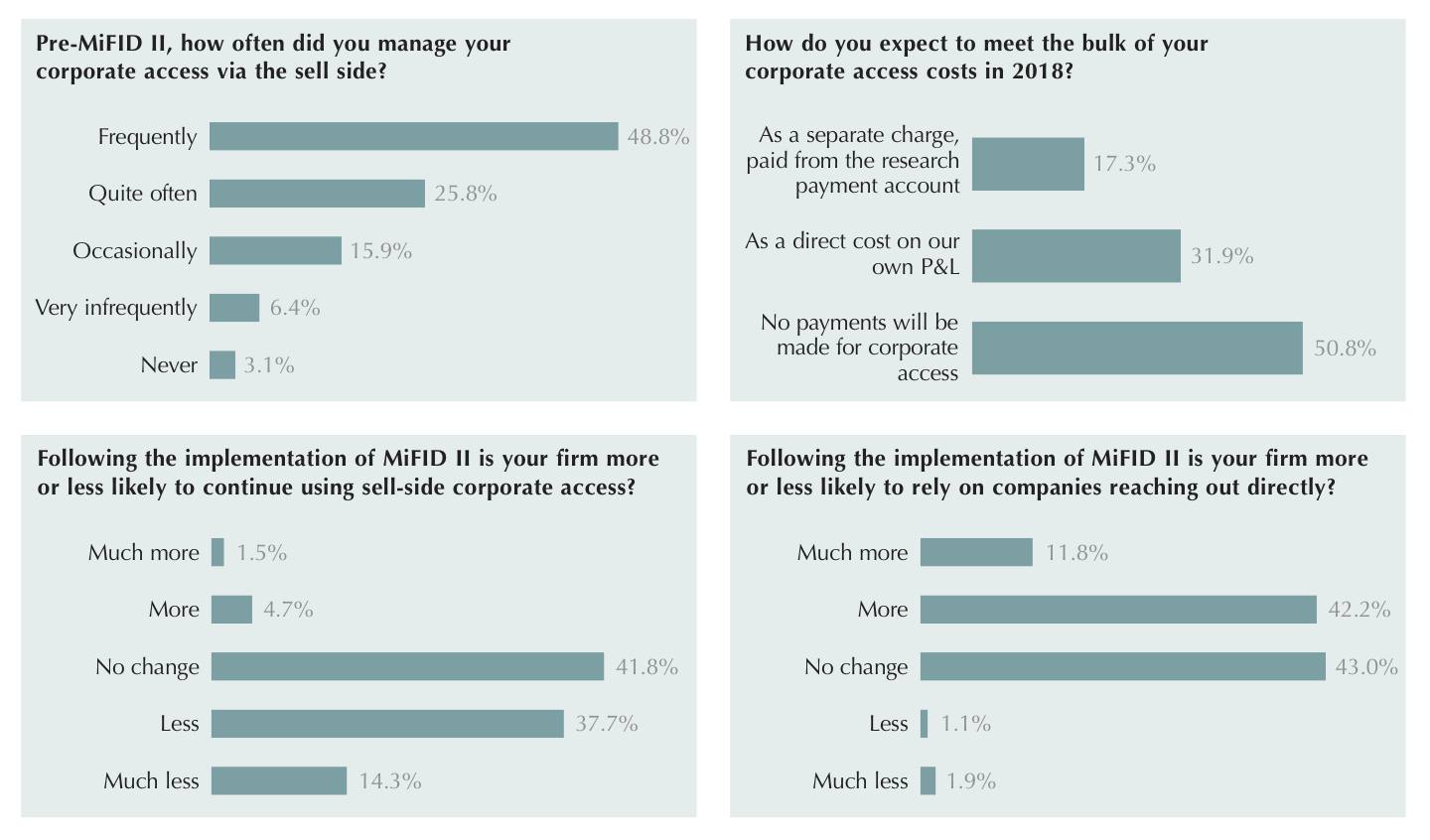

Before the implementation date, 90% of investors were regularly using corporate access services provided by the sell side, with 49% saying they did so frequently. In contrast, only 38% of investors were regularly reliant on companies contacting them directly.

Reduced access is not an option

Maintaining corporate access post-MiFID II is clearly essential for the large majority of investors, with 92% saying that it is important to their investment process and 43% stating that it is critical. It is therefore unsurprising that most do not expect their level of corporate access to reduce. In fact, 75% of investors expect to meet company management just as much, or more, than they have done prior to MiFID II.

The question of payment

Investors are evenly split on this. 51% do not intend to pay for corporate access; however, 32% plan to cover corporate access charges as a direct cost on their P&L. 17% told us that they will pay a separate charge for access, from their research payment account.

Widespread discontent

Many investors feel strongly that they should not have to pay for corporate access:

“Brokers will have to charge, and I refuse to pay, particularly when I am a shareholder already!”

Even among investors who do expect to pay, there are clearly concerns about the burden of additional costs:

“For a small company like us, to have to pay to get corporate access is a killer.”

Balance set to change

The most obvious way for investors to avoid paying for corporate access, is if meetings are arranged between companies and investors directly. The likely shift is clear: 52% say they will use the sell side less for corporate access in future, while 54% said they will be more reliant on companies reaching out to them.

“We would like to see far less reliance on the sell side as corporate access intermediaries by companies. We also believe companies would benefit from a better relationship with their shareholders if this occurred.”

Roadshows still preferred

Non-deal roadshows remain the preferred way to meet with companies. 59% of investors say that this is their number one preference in comparison to alternatives such as reverse roadshows (18%) or conferences (16%).

The way forward

With a significant number of investors expecting the sell side to be less involved in corporate access, the onus is shifting to IR teams to take an increasingly proactive role in planning roadshows and scheduling meetings.

The majority of investors anticipate that companies will either increase their internal IR resource or begin to use independent corporate access providers instead.

“Well-managed companies will improve their direct communications, increasing the quality and number of IR staff.”

“I believe companies will pay independent corporate access services to organise their roadshows rather than using brokers at no cost.”

Conclusion

Much attention has been paid to the implications for research distribution under MiFID II. However, from an IR perspective the impact on corporate access is likely to be equal or even greater.

Given the need for investors to demonstrate compliance with the regulations, as well as the pressure on margins for fund management, it is no surprise that so many investors are now looking to corporates to maintain proactive interaction.

John Gollifer, general manager of the IR Society, added: “This timely survey suggests that the responsibility for investor engagement is shifting inexorably to the companies themselves. The changes wrought by increasingly regulated public capital markets mean that we will see a need for, if not an onus on, company management to ensure that its investor communications is properly resourced and ready to fill any gaps that appear in the investment process of investors. I have no doubts that listed companies themselves, through their IR teams, will have to be proactive, step up and be the vital link between their business and their investors.”

Charles Hamlyn is founder and managing director of QuantiFire.

Published 27 March, 2018